Getting Started¶

Setup¶

python3 -m venv .venv

source .venv/bin/activate

pip install mellow_strategy_sdk

The easiest way to get started is to use SDK examples in the Github repo.

Import¶

from mellow_sdk.primitives import Pool, POOLS

from mellow_sdk.data import RawDataUniV3

from mellow_sdk.strategies import AbstractStrategy

from mellow_sdk.backtest import Backtest

from mellow_sdk.viewers import RebalanceViewer, UniswapViewer, PortfolioViewer

from mellow_sdk.positions import BiCurrencyPosition, UniV3Position

Choose a pool¶

A typical notebook would start with downloading and preparing data for a specific pool.

POOLS is a list of available pools, let’s choose 1 it is WBTC/WETH, fee 0.3%

pool_num = 1

pool = Pool(

tokenA=POOLS[pool_num]['token0'],

tokenB=POOLS[pool_num]['token1'],

fee=POOLS[pool_num]['fee']

)

Get data¶

Аt the first run you need to download the data

data = RawDataUniV3(pool, 'data', reload_data=False).load_from_folder()

Create strategy¶

class UniV3Passive(AbstractStrategy):

"""

``UniV3Passive`` is the passive strategy on UniswapV3, i.e. mint one interval and wait.

Attributes:

lower_price: Lower bound of the interval

upper_price: Upper bound of the interval

gas_cost: Gas costs, expressed in currency

pool: UniswapV3 Pool instance

name: Unique name for the instance

"""

def __init__(self,

lower_price: float,

upper_price: float,

pool: Pool,

gas_cost: float,

name: str = None,

):

super().__init__(name)

self.lower_price = lower_price

self.upper_price = upper_price

self.fee_percent = pool.fee.percent

self.gas_cost = gas_cost

self.swap_fee = pool.fee.percent

def rebalance(self, *args, **kwargs) -> str:

# record is row of historic data

record = kwargs['record']

# portfolio managed by the strategy

portfolio = kwargs['portfolio']

price_before, price = record['price_before'], record['price']

is_rebalanced = None

if len(portfolio.positions) == 0:

self.create_uni_position(portfolio=portfolio, price=price)

is_rebalanced = 'mint'

if 'UniV3Passive' in portfolio.positions:

uni_pos = portfolio.get_position('UniV3Passive')

# collect fees from uni

uni_pos.charge_fees(price_before, price)

return is_rebalanced

def create_uni_position(self, portfolio, price):

x = 1 / price

y = 1

# create biccurency positions for swap

bi_cur = BiCurrencyPosition(

name=f'main_vault',

swap_fee=self.swap_fee,

gas_cost=self.gas_cost,

x=x,

y=y,

x_interest=None,

y_interest=None

)

# create uni interval

uni_pos = UniV3Position(

name=f'UniV3Passive',

lower_price=self.lower_price,

upper_price=self.upper_price,

fee_percent=self.fee_percent,

gas_cost=self.gas_cost,

)

portfolio.append(bi_cur)

portfolio.append(uni_pos)

# get tokens amount to swap

dx, dy = uni_pos.aligner.get_amounts_for_swap_to_optimal(

x, y, swap_fee=bi_cur.swap_fee, price=price

)

# swap

if dx > 0:

bi_cur.swap_x_to_y(dx, price=price)

if dy > 0:

bi_cur.swap_y_to_x(dy, price=price)

x_uni, y_uni = uni_pos.aligner.get_amounts_after_optimal_swap(

x, y, swap_fee=bi_cur.swap_fee, price=price

)

# withdraw tokens from bicurrency

bi_cur.withdraw(x_uni, y_uni)

# deposit tokens to uni

uni_pos.deposit(x_uni, y_uni, price=price)

Typycally the definition of the rebalance method would contain two sections:

- Init

On the first call you need to initialize strategy’s portfolio under management. Here you create initial positions at

create_uni_positionandappendtoPortfolio

- Rebalance

In this section you decide if you want to rebalance or not. If you rebalance you need to implement the logic of rebalance.

Backtest¶

Next step is to run backtest using your strategy and data

univ3_passive = UniV3Passive(

lower_price=data.swaps['price'].min(),

upper_price=data.swaps['price'].max(),

pool=pool,

gas_cost=0.,

name='passive'

)

bt = Backtest(univ3_passive)

portfolio_history, rebalance_history, uni_history = bt.backtest(data.swaps)

Visualize¶

Next visualize results

rv = RebalanceViewer(rebalance_history)

uv = UniswapViewer(uni_history)

pv = PortfolioViewer(portfolio_history, pool)

# Draw portfolio stats, like value, fees earned, apy

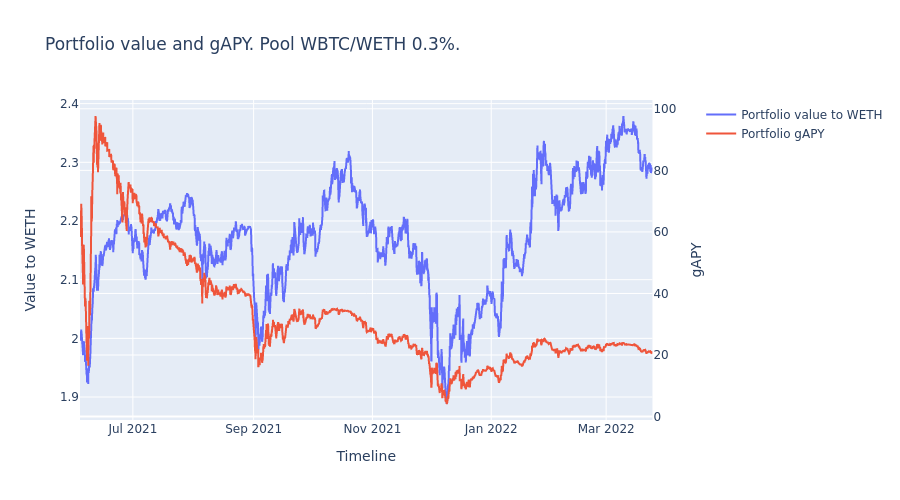

fig1, fig2, fig3, fig4, fig5, fig6 = pv.draw_portfolio()

# Draw Uniswap intervals

intervals_plot = uv.draw_intervals(data.swaps)

# Draw rebalances

rebalances_plot = rv.draw_rebalances(data.swaps)

# Calculate df with portfolio stats

stats = portfolio_history.calculate_stats()

intervals_plot.show()

rebalances_plot.show()

fig2.show()

fig4.show()

fig6.show()

stats.tail(2)

timestamp |

price |

total_value_x |

total_value_y |

total_il_to_x |

total_il_to_y |

total_fees_x |

total_fees_y |

total_value_to_x |

total_value_to_y |

total_fees_to_x |

total_fees_to_y |

hold_to_x |

hold_to_y |

portfolio_apy_x |

portfolio_apy_y |

hold_apy_x |

hold_apy_y |

g_apy |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

2022-03-24T18:26:04.007000000 |

14.145663861009012 |

0.08402850645482046 |

1.1006858710370173 |

0.0024166183368408145 |

0.03418467067330111 |

0.013526451868427254 |

0.19623228970023882 |

0.16183933822998647 |

2.2893248780895337 |

0.027398709234950136 |

0.38757293106312807 |

0.1368572473318771 |

1.9359366176997062 |

34.33642131128549 |

16.58755840478303 |

11.149908316373637 |

-3.535494685439844 |

20.86057770638414 |

2022-03-24T18:38:08.496000000 |

14.146024071596418 |

0.08402068238281096 |

1.100796881173142 |

0.002415605901264717 |

0.034171219226781124 |

0.013526451868427254 |

0.19623262173454428 |

0.16183738024800226 |

2.289355476672343 |

0.02739837946740234 |

0.38757813546860653 |

0.1368546066818646 |

1.9359485604305164 |

34.33458473753552 |

16.5893193133706 |

11.147484822368092 |

-3.53482221907514 |

20.861560612212003 |

Congratulations! Now you have the results of your strategy backtest on the real UniV3 data!